Addressing popular MakerDAO criticisms

Quick Take

- Preston Byrne’s persistent critiques have motivated an attempt to clarify some popular misunderstandings around MakerDAO’s mechanisms

- This piece also seeks to provide ‘better criticisms’ of the MakerDAO system

Preston Byrne, attorney at Bryne & Storm, P.C, is a notable critic of Ethereum, Open Finance, and, specifically, MakerDAO. I often find myself taking exception to his empirical misunderstandings of the MakerDAO mechanics. This piece seeks to address some of these misunderstandings.

Byrne’s MakerDAO criticisms can be synthesized into the following five categories:

1. MakerDAO is (perhaps purposefully) confusing

2. MakerDAO is not resistant to Black Swans

3. Dai only works if the value of ether increases in perpetuity

4. Generating Dai is capital inefficient

5. The peg is maintained by a mix of ‘magic’ and market makers

1. MakerDAO is (perhaps purposefully) confusing

Stablecoins are doomed to fail:

Having taken fifteen minutes to review the MakerDAO paper, the Dai system is at its core a very simple cryptocurrency-collateralised derivative contract, with a lot of intermediate steps to confuse its buyers of the fact that...the contract is massively overcollateralized in the underlying cryptocurrency (which is Ethereum by default)

Preston is correct in his description of the MakerDAO system as a series of cryptocurrency collateralized derivative contracts.

The clue, perhaps, is in the name that that MakerDAO has assigned to these contracts — Collateralized Debt Positions. Currently a user wishing to open a CDP must indeed overcollateralize by 150% — for every $150 of ether deposited as collateral, $100 worth of Dai can be minted: this collateral margin is designed to protect Dai holders against a negative equity scenario.

To be sure, MakerDAO is a complex system with various moving parts — the MKR token, Dai, CDPs, Stability Fees, Dai Savings Rates, oracles and more. But complexity should not be conflated with impracticality. Buying, holding, and using Dai does not necessarily require a deep understanding of MakerDAO’s mechanics, in the same way that buying and holding and using U.S. dollars does not require a particularly strong grasp on monetary economics.

2. MakerDAO is not resistant to Black Swans

In the event of an Ethereum black swan event the value of the underlying collateral, and therefore the value of the stablecoin, will also be wiped out.

The Black Swan argument is as follows: Ethereum may suffer from some catastrophic bug or a regulatory crackdown, at which point the value and liquidity of ether plummets before the collateral backing Dai can be liquidated.

I concede this point to Byrne, although I simultaneously take issue with assessing the merits of a project based on Black Swan events — indeed, there are few products or enterprises that are not susceptible to some form of Black Swan. Taken to its extreme, Preston’s logic would suggest that there is little reason to do anything, ever, due to the infinitesimal-yet-possible chance that a Black Swan event occurs. A superior framework is Value at Risk.

MakerDAO’s system does have some protection against undercollateralization in the form of the MKR token, which serves as something akin to a Credit Default Swap, alongside its voting properties. In the event that the system enters an undercollateralized state, MKR supply is programmatically inflated and sold on the market, with any returns directed towards Dai holders. While not infallible — there is no guarantee that the MKR market will have sufficient liquidity in the event of an Ethereum ‘black swan’ — this CDS-type protection does provide an additional margin of safety for Dai holders.

Indeed, one further concern is a liquidity crunch in the Dai market in the event of deleveraging spiral, as described in the Ariah Klages-Mundt and Andreea Minca’s recent paper, (In)Stability for the Blockchain: Deleveraging Spirals and Stablecoin Attacks. Klages-Mundt and Minca describe a scenario where CDP holders rush en masse to close out their positions when ether is falling precipitously, thereby bidding up the price of Dai. At certain Dai price levels, CDP holders may not have sufficient funds to cover their debt positions, leading to further vicious cycle of liquidations.

MakerDAO’s imminent transition to a multi-collateral portfolio, expected to launch in Q4 2019, should mitigate some of these issues: a diverse collateral portfolio mitigates system-wide risk in the event that one collateral type suffers from rapid price depreciation. Importantly, MakerDAO stakeholders (i.e. MKR holders) must tailor risk parameters — debt ceilings, collateralization ratios, liquidation discounts — according to the liquidity of collateral spot markets. Ether currently has a relatively conservative debt ceiling of 100 million Dai (i.e a maximum of 100 million Dai can be generated from ether collateral), alongside a 150% collateralization ratio and 12% liquidation penalty. Ether currently commands a $20 billion market cap and regularly sees multiple hundred million-dollar daily volume.

3. Dai only works if the value of ether increases in perpetuity

This system makes zero sense and is broken to the core: it only works if the price of Ether goes up. Cognizant that the conventional wisdom is that the Ethereum “World Computer’s” price will always go up, and it has done nothing but go up for the last 18 months, I can see how this might make sense to the MakerDAO team.

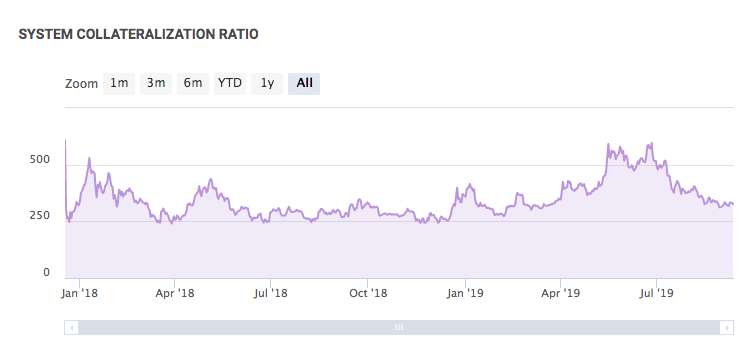

Data speaks for itself, so I leave you with the following charts - the first showing MakerDAO systemwide collateralization ratio since inception, the second showing ether/USD price activity over the same period.

Source: mkr.tools

Source: tradingview.com

Having said that, the system does naturally provide more utility as the price of ether appreciates in that more Dai can be generated from a more valuable collateral pool. Fortunately, additional collateral types can take some pressure off reliance on ether appreciation.

4. Generating Dai is capital inefficient

Speaking generally, the system requires someone who wishes to obtain $100 worth of Dai to post, say, $150 Ethers’ worth of collateral. This, of course, is insane, because it would be easier for the user to simply go to Coinbase and sell his Ether for actual dollars, and he’d have $50 worth of Eth left over to go spend on other things.

This is an accurate description of the CDP process.

This is, however, not ‘insane’ for any person familiar with margin trading, which requires speculators to deposit some margin in order to leverage long or short a particular asset. With a 33% margin requirement, CDPs allow ether holders to 3x long — that is, by borrowing Dai and selling it for more Ether, one can turn $150 worth of Ether exposure into $450 worth of exposure. A mortgage, in which a homeowner borrows against the value of their property, is somewhat analogous. As of Q1 2019, there is approximately $15 trillion worth of outstanding mortgage debt in the U.S. alone.

Like other collateralized loans — CDPs permit ether holders to tap into the equity value of their asset while maintaining long exposure and without generating an immediate taxable event — this is particularly relevant in jurisdictions like the U.S., where the tax system differentiates between short- and long-term capital gains.

Capital efficiency may also naturally improve under Multi-Collateral Dai. According to Placeholder Capital's report published in March, the median collateralization ratio of liquidated CDPs is 149.5%, suggesting existing constraints can be relaxed. dYdX, a secondary lending platform, currently requires a minimum 115% collateralization ratio and, to date, none of their users have entered into a state of negative equity.

5. The peg is maintained by a mix of ‘magic’ and market makers

Stablecoins are doomed to fail, Part II: MakerDAO’s “DAI” stablecoin is breaking, as predicted

Long have I been a critic of the “stablecoin” concept – the techno-magical idea that a cryptocurrency can tell the market what its price should be, rather than the market determining what a cryptocurrency’s price should be (the usual way these things work).

The concept of monetary policy has existed since the creation of the Bank of England in 1694: “The goal of monetary policy was to maintain the value of the coinage, print notes which would trade at par to specie, and prevent coins from leaving circulation.”

MakerDAO stakeholders vote on and adjust the Stability Fee — analogous to interest rates — on a weekly basis. This Stability Fee ensures that Dai achieves its soft peg target of $1. If Dai is trading below the dollar, Stability Fees are adjusted upwards, increasing the cost to borrow and encouraging borrowers to close their debt and take Dai out of the system. This reduction in circulating Dai supply helps the market return to an equilibrium price where Dai trades at par with the U.S. dollar. Conversely, when Dai is trading above $1, Stability Fees are lowered, reducing the cost to borrow and encouraging further generation of Dai supply. The entrance of additional Dai onto the market creates sufficient sell pressure to bring Dai back down to $1.

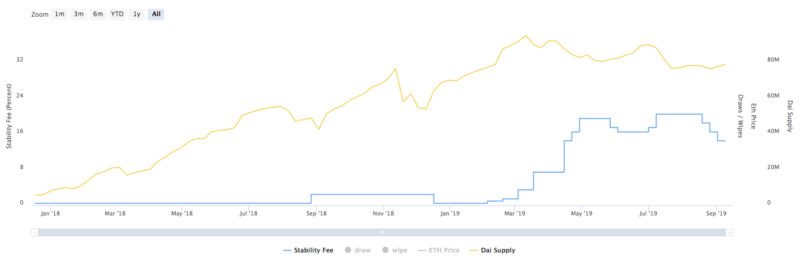

To date, these Stability Fee adjustments have proven to effectively influence CDP user behaviour: the chart below illustrates a high degree of inverse correlation between the Stability Fee and Dai supply.

Source: mkr.tools

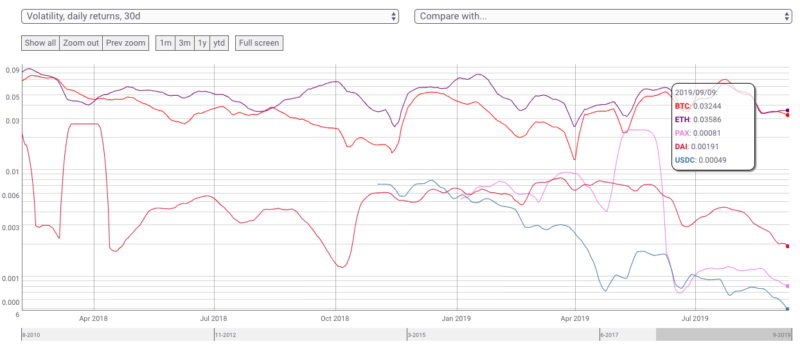

Brief deviations from the peg are to be expected, especially at the beginning of MakerDAO’s life cycle, as market forces drive Dai away from its target $1 value. More recently we have seen Dai volatility dampen as market participants become increasingly familiar with the underlying mechanics of MakerDAO and, resultantly, bid up Dai when it slips below its peg and sell mint and sell Dai when it drifts upwards — “your margin call is my opportunity”.

Source: coinmetrics.io

Additionally, value assigned to maintaining a perfectly constant peg to USD is perhaps misguided: Dai is ultimately a means for counterparties to trade volatility and to date it has successfully minimized volatility relative to ether.

As for market makers:

Welp, it turns out that was a pretty good guess: the only reason the DAI “stablecoin” was stable is because a bot was wash trading most of the volume in the markets back and forth around the $1.00 mark.

Preston seems to take issue with market makers, who provide liquidity while capturing spreads. Market makers operate at volume in the Dai market. That this is the case is a) a positive for the MakerDAO ecosystem b) a signal of faith in the MakerDAO mechanisms.

To this second point — market makers necessarily have to hold inventory in order to participate on the ‘ask’ side of the market. If the expectation was that the value of Dai could collapse at any time, we would probably not see considerable market maker activity in the Dai market. This inventory risk is why cryptocurrencies with dubious value accrual mechanism often suffer from illiquid markets.

Better criticisms!

The Ethereum community often notes that they need better critics. Similarly, MakerDAO needs more nuanced critics. While the system has functioned well to date, it is certainly not infallible.

Possible lines of criticism include the following:

1. The oracle system that ensures the system remains overcollateralized is far from trustless. The existing implementation relies on a dozen or so MakerDAO stakeholders, who intermittently post price feeds on chain: MakerDAO then takes a median of these prices. This is clearly not perfect, although it is sufficient while more robust solutions, such as Dan Robinson’s Bounded Protocol, undergo development and testing.

2. There is no natural arbitrage cycle for when Dai drifts above its peg. Hasu and Su Zhu cogently outline this phenomenon here.

3. In its existing form, MKR does not serve as a pseudo-CDS — in the event of under collateralization, Dai holders will not be protected by programmatic selling of MKR. A corollary here is that MKR holders are currently free-riding on the MakerDAO system in that they are rewarded with MKR burns while not taking on any risk.

4. Candidates for multi-collateral Dai remain scarce. This is not an impossible problem and risk parameters can be carefully tailored towards particular asset liquidity and market cap, but at present the path to scaling Dai to a multi-billion dollar market cap is not particularly clear.

5. It seems unlikely that the U.S. Treasury will stand by as MakerDAO stakeholders create and grow a synthetic dollar system. Similarly, MKR may have some hallmarks of a security.

6. Today’s Stability Fee adjustments are driven by a fairly rudimentary process. This is not to criticize those involved in MakerDAO’s Risk & Governance process — ultimately they are operating to the best of their ability. Rather, today’s markets are inefficient and volatile and accurately predicting, let alone quantifying, market forces remains a quandary. The emergence of a Dai yield curve through Yield Protocol may alleviate some of these issues.

7. MKR, which is used to participate in various network votes, is currently fairly concentrated. Although the Maker Foundation has suggested that they will not participate in governance themselves, they do currently control just over 25% of outstanding MKR tokens. Crypto investment funds Polychain Capital and a16z crypto also own large stakes in MKR. Although there are protections in place — namely the Emergency Shutdown feature — to prevent large MKR holders from abusing the network, this concentration of supply may prove to be politically sensitive.

8. The Maker Foundation, a non-profit body that, among various activities, develops the MakerDAO network, is a possible single point of failure. The Maker Foundation could feasibly be pressured by regulatory authorities to trigger Emergency Shutdown and it remains an open question as to whether risk, governance, and development activities can be sustained without their support.

The nice thing about Dai is that it has a relatively liquid lending market. If you, or Preston, thinks that Dai is going to collapse to no return, it might be sensible to short it.

© 2023 The Block. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.